Market Update: Balancing acts

Matt, UK not looking forward to the Autumn Budget, 28 August 2024

Balancing acts

While markets appeared to go sideways, underneath the surface there has actually been a remarkable change in dynamics.

Why investors look so much to the US

The US market makes up 61% of the world’s stock market, but the US’s share of the global economy has been declining for decades, so why are investment professional so US focussed?

Easing liquidity tightness made in China?

China would have benefitted from easier monetary policy, but politics got in the way. Now that the renminbi has strengthened against the US$ this should change for the better.

Balancing acts

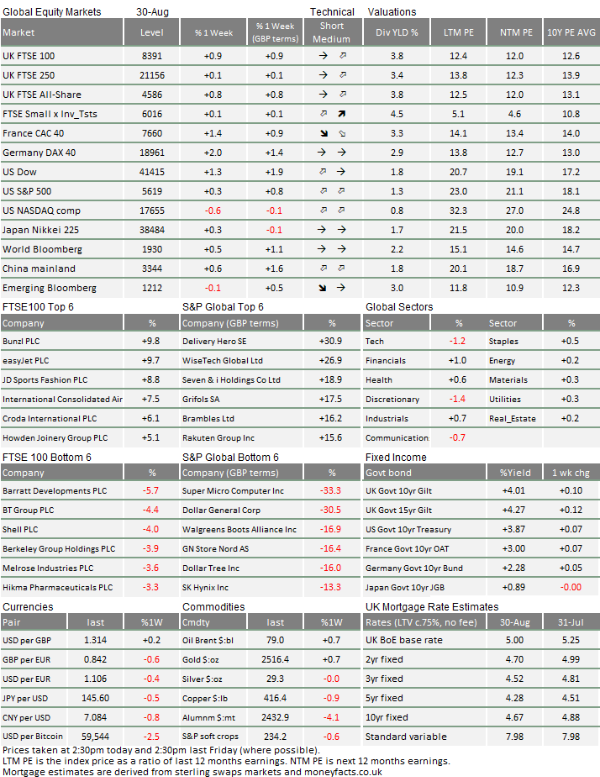

It was a flat week for global stock values, but with a fair amount of dispersion. US returns were once again weighed down by tech, but the UK and Europe are up over 1% at the time of writing. The overall sluggish picture seems a strange reaction to supportive comments from US Federal Reserve chair Powell and a healthier than expected US economy, but markets are chewing on a few things.

UK investors suspect a hike in Capital Gains Tax (CGT), possibly among other measures, in the government’s autumn budget. Anecdotal evidence suggests this is keeping advisers very busy – and some have predicted UK market consternation.

There was certainly no sign of that in UK stock values. Individual investors may want to realise gains now, but either for immediate reinvestment or medium-term spending purposes. We have argued before that readily available CGT investment wrappers mitigate CGT changes. Underlying fundamentals are more important, and those probably will not be greatly affected by the budget. We will of course keep an eye on this, but return for now to some more globally impactful news.

Markets seem to be more like their pre-pandemic selves, after many ups and downs. It’s difficult to distinguish the permanent changes from the reactionary ones, but many strongly impacted areas are now more than fully recovered – evidenced by the travel industry’s new high in air miles. Interest rates and bond yields, however, are more like where they were before the Great Financial Crisis. We think a return to pre-pandemic levels, rather than pre-GFC, is more likely. Yields are likely to go down, even though they were up last week.

A doubling of profits isn’t enough to bring in new Nvidia investors.

Ahead of AI market leader Nvidia’s earnings, commentators heralded that the chipmaker’s results are as important to markets as major economic data. In the event, Nvidia announced $30 billion in revenue in the three months to August – up 122% from a year earlier – and expects $32.5bn for the third quarter. Shares in the company then dropped 6% on Thursday, despite beating analyst expectations.

Disappointment may have stemmed from the fact it was Nvidia’s smallest revenue surprise in six quarters. Investors are so accustomed to its freakishly good results that very good is not enough. This is less about the company itself and more a realisation that AI-related investments may have run a little too hot.

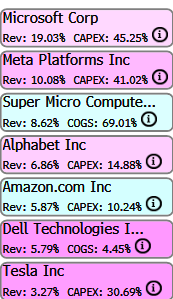

We note that Wednesday’s news regarding Super Micro Computer (SMC) had already set the scene. SMC has been central in the AI stock theme: it went from a market capitalisation of $4bn in January 2023 to $66bn in mid-March this year. As of the close last night, it was back to $26.2bn.

For Nvidia, SMC has been a major buyer of the H100, the current flagship GPU chip. According to Bloomberg analysis, SMC was Nvidia’s third largest customer over the past year, forming 8.6% of revenue, as the table to the right shows.

SMC’s shares dropped 19%, after being targeted by infamous short-seller Hindenburg Research. Hindenburg alleges that SMC manipulated its accounts. These allegations seriously damage the optimism needed to invest in long-term themes. The timing was awful for Nvidia, meaning good results weren’t enough and new buyers want a cheaper stock price.

Thankfully, the S&P 500 did not follow Nvidia’s lead. It ended Thursday slightly down but started brightly, thanks to some positive economic data. This is a decent sign – suggesting faith in the broad economy even if mega-cap valuations are a little stretched.

After the central bankers’ Jackson Hole conference the weekend before last, markets are more focused on what central banks do. The key question right now is…

Are interest rates currently restrictive?

In his speech the weekend before last, Fed chair Jay Powell reemphasised a focus on employment, more than inflation. Subsequently, bets on a 0.5% rate cut in September – rather than the 0.25% currently priced in – went up. Bond markets currently suggest around a third chance of 0.5% next month, but we actually think it is more of a 50/50.

There are suggestions that this is unnecessary and could either stoke market fears about the economy or increase inflation. We have said all along that the US economy is in a decent position: consumption is solid, while there are no signs of systemic credit stress. Does the world’s largest economy really need sharply lower rates?

“Need” is too strong, but cuts are certainly appropriate. The point is not that the economy is in distress, but that risks have risen markedly. Unemployment has increased slowly but is now at a point where it could quickly spiral if left unchecked and smaller businesses have clearly not been doing well for some time.

Firms have been reluctant to lay off employees – probably because they remember how hard it was to hire post-covid. That could change. Swedish fintech firm Klarna made headlines last week by announcing it would replace workers with AI – which feels like an ominous sign. If that becomes a trend, unemployment could get nasty quick.

In the UK and Europe, growth seems to be a little steadier, possibly because it was not so stellar before. Labour markets are easing at a gentler pace. ECB and Bank of England rate-setters have suggested that rates can come down, but it is not definite. We are pretty sure that rates will be cut again this year and into next, judging by currency strength.

Markets are right to ignore the election.

Curiously, markets recently seem completely unmoved by US election drama. Some will tell you that US or global asset values are relatively unaffected by who is in the White House, but we have plenty of evidence to the contrary. This election clearly matters for stocks: Donald Trump and Kamala Harris have vastly different plans for corporate tax, and we have argued that Trump carries a bigger threat to bond markets too.

Markets recognised how impactful the election result could be at the start of July, when the odds of a Trump victory peaked and investors got excited about tax cuts for small and mid-cap companies. But now, markets are acting as though it makes no difference.

This is because the outcomes are so uncertain and ripe for biased estimation, that it makes sense to treat them as irrelevant – which they clearly are not. The election is on a knife edge in terms of forecasts and betting markets (polls give Harris the lead, but the popular vote doesn’t guarantee the presidency).

The big picture implications of either candidate’s policies are unclear. Trump will cut taxes and boost short-term US profit growth, at the expense of global trade and possibly long-term fiscal stability. Harris might eat into corporate profit margins, but will probably continue the status quo and might boost long-term growth through government sponsored investment. Markets think neither of these scenarios are ideal, but it is hard to work out which is better.

Markets are also notoriously bad at reacting to elections. They tend to react when big surprises happen, but overestimate both the policy impacts of certain candidates and the economic or financial impacts of those. Election-inspired sell-offs usually make good buying opportunities for that reason – with Trump’s 2016 win being a classic example.

With less than seven weeks to go, commentators have pointed out that a significant proportion of US voters will have probably decided which candidate they want, and news is not likely to change their preference. What matters is whether they actually vote, which we won’t know until the day itself. Given all that, it is reasonable to ignore the US election campaign and wait for bonfire night.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.